More Copula stuff coming again. This time, I wanted to open my implementation for Basket Default Swap (BDS) pricer. It is assumed, that the reader is familiar with this exotic credit product.

The core of the program is BasketCDS class, which is performing the actual Monte Carlo process. This class is using NAGCopula class for creating correlated uniform random numbers needed for all simulations. It also uses CreditCurve class for retrieving credit-related data for calculating default times. Finally, it holds a delegate method for desired discounting method. For storing the calculated default and premium leg values, delegate methods are used to send these values to Statistics class, which then stores the both leg values into its own data structures. In essence, BasketCDS class is doing the calculation and Statistics class is responsible for storing the calculated values and reporting its own set of desired (and configured) statistics when requested.

As already mentioned, CreditCurve class is holding all the credit-related information (CDS curve, hazard rates, recovery rate). DiscountCurve class holds the information on zero-coupon curve. In this class, discounting and interpolation methods are not hard-coded inside the class. Instead, the class is holding two delegate methods for this purpose. The actual implementations for the both methods are stored in static MathTools class, which is nothing more than just collection of methods for different types of mathematical operations. Some matrix operations are needed for handling matrices when calculating default times in BasketCDS class. For this purpose, static MatrixTools class is providing collection of methods for different types of matrix operations. Needless to say, new method implementations can be provided for concrete methods used by these delegates.

Source market data (co-variance matrix, CDS curve and zero-coupon curve) for this example program has been completely hard-coded. However, with the examples presented in here or in here, the user should be able to interface this program back to Excel, if so desired.

The client example program is calculating five fair spreads for all kth-to-default basket CDS for all five reference names in the basket. In a nutshell, Monte Carlo procedure to calculate kth-to-default BDS spread is the following.

In order to run this program, one needs to create a new C# console project and copyPaste the program given below into a new cs file. It is also assumed, that the user is a registrated NAG licence holder. Other users have to provide their own implementation for Copula needed in this program or use my implementation. With the second approach, a bit more time will be spent in adjusting this program for all the changes required.

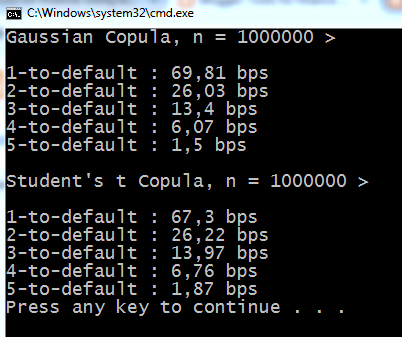

Results for one test run for the both Copula models is presented in the following console screenshot.

![]()

Observed results are behaving as theory is suggesting. BDS prices are decreasing as more reference names are needed for triggering the actual default. Also, tail-effect created by the use of Student Copula model is captured as higher prices after 1st-to-default BDS. Computational help provided by NAG G05 library is just amazing. After you outsource the handling of Copula model for external library, there is not so much to program either.

That is all I wanted to share with you this time. Thanks for reading my blog. Mike.

PROGRAM DESIGN

The core of the program is BasketCDS class, which is performing the actual Monte Carlo process. This class is using NAGCopula class for creating correlated uniform random numbers needed for all simulations. It also uses CreditCurve class for retrieving credit-related data for calculating default times. Finally, it holds a delegate method for desired discounting method. For storing the calculated default and premium leg values, delegate methods are used to send these values to Statistics class, which then stores the both leg values into its own data structures. In essence, BasketCDS class is doing the calculation and Statistics class is responsible for storing the calculated values and reporting its own set of desired (and configured) statistics when requested.

As already mentioned, CreditCurve class is holding all the credit-related information (CDS curve, hazard rates, recovery rate). DiscountCurve class holds the information on zero-coupon curve. In this class, discounting and interpolation methods are not hard-coded inside the class. Instead, the class is holding two delegate methods for this purpose. The actual implementations for the both methods are stored in static MathTools class, which is nothing more than just collection of methods for different types of mathematical operations. Some matrix operations are needed for handling matrices when calculating default times in BasketCDS class. For this purpose, static MatrixTools class is providing collection of methods for different types of matrix operations. Needless to say, new method implementations can be provided for concrete methods used by these delegates.

Source market data (co-variance matrix, CDS curve and zero-coupon curve) for this example program has been completely hard-coded. However, with the examples presented in here or in here, the user should be able to interface this program back to Excel, if so desired.

MONTE CARLO PROCESS

The client example program is calculating five fair spreads for all kth-to-default basket CDS for all five reference names in the basket. In a nutshell, Monte Carlo procedure to calculate kth-to-default BDS spread is the following.

- Simulate five correlated uniformly distributed random numbers by using Gaussian or Student Copula model.

- Transform simulated five uniform random numbers to default times by using inverse CDF of exponential distribution.

- By using term structure of hazard rates, define the exact default times for all five names.

- Calculate the value for default leg and premium leg.

- Store the both calculated leg values.

- Repeat steps from one to five N times.

- Finally, calculate BDS spread by dividing average of all stored default leg values with average of all stored premium leg values.

In order to run this program, one needs to create a new C# console project and copyPaste the program given below into a new cs file. It is also assumed, that the user is a registrated NAG licence holder. Other users have to provide their own implementation for Copula needed in this program or use my implementation. With the second approach, a bit more time will be spent in adjusting this program for all the changes required.

Results for one test run for the both Copula models is presented in the following console screenshot.

Observed results are behaving as theory is suggesting. BDS prices are decreasing as more reference names are needed for triggering the actual default. Also, tail-effect created by the use of Student Copula model is captured as higher prices after 1st-to-default BDS. Computational help provided by NAG G05 library is just amazing. After you outsource the handling of Copula model for external library, there is not so much to program either.

That is all I wanted to share with you this time. Thanks for reading my blog. Mike.

THE PROGRAM

using System;

using System.Collections.Generic;

using System.Linq;

using System.Text;

using NagLibrary;

//

namespace BasketCDSPricer

{

// delegates for updating leg values

publicdelegatevoid PremiumLegUpdate(double v);

publicdelegatevoid DefaultLegUpdate(double v);

//

// delegate methods for interpolation and discounting

publicdelegatedouble InterpolationAlgorithm(double t, refdouble[,] curve);

publicdelegatedouble DiscountAlgorithm(double t, double r);

//

//

// *************************************************************

// CLIENT PROGRAM

classProgram

{

staticvoid Main(string[] args)

{

try

{

// create covariance matrix, discount curve, credit curve and NAG gaussian copula model

double[,] covariance = createCovarianceMatrix();

DiscountCurve zero = new DiscountCurve(createDiscountCurve(),

MathTools.LinearInterpolation, MathTools.ContinuousDiscountFactor);

CreditCurve cds = new CreditCurve(createCDSCurve(), zero.GetDF, 0.4);

NAGCopula copula = new NAGCopula(covariance, 1, 1, 2);

//

// create containers for basket pricers and statistics

// set number of simulations and reference assets

List<BasketCDS> engines = new List<BasketCDS>();

List<Statistics> statistics = new List<Statistics>();

int nSimulations = 250000;

int nReferences = 5;

//

// create basket pricers and statistics gatherers into containers

// order updating for statistics gatherers from basket pricers

for (int kth = 1; kth <= nReferences; kth++)

{

statistics.Add(new Statistics(String.Concat(kth.ToString(), "-to-default")));

engines.Add(new BasketCDS(kth, nSimulations, nReferences, copula, cds, zero.GetDF));

engines[kth - 1].updateDefaultLeg += statistics[kth - 1].UpdateDefaultLeg;

engines[kth - 1].updatePremiumLeg += statistics[kth - 1].UpdatePremiumLeg;

}

// run basket pricers and print statistics

engines.ForEach(it => it.Process());

statistics.ForEach(it => it.PrettyPrint());

}

catch (Exception e)

{

Console.WriteLine(e.Message);

}

}

//

// hard-coded co-variance matrix data

staticdouble[,] createCovarianceMatrix()

{

double[,] covariance = newdouble[5, 5];

covariance[0, 0] = 0.001370816; covariance[1, 0] = 0.001113856; covariance[2, 0] = 0.001003616;

covariance[3, 0] = 0.000937934; covariance[4, 0] = 0.00040375;

covariance[0, 1] = 0.001113856; covariance[1, 1] = 0.001615309; covariance[2, 1] = 0.000914043;

covariance[3, 1] = 0.000888594; covariance[4, 1] = 0.000486823;

covariance[0, 2] = 0.001003616; covariance[1, 2] = 0.000914043; covariance[2, 2] = 0.001302899;

covariance[3, 2] = 0.000845642; covariance[4, 2] = 0.00040185;

covariance[0, 3] = 0.000937934; covariance[1, 3] = 0.000888594; covariance[2, 3] = 0.000845642;

covariance[3, 3] = 0.000954866; covariance[4, 3] = 0.000325403;

covariance[0, 4] = 0.00040375; covariance[1, 4] = 0.000486823; covariance[2, 4] = 0.00040185;

covariance[3, 4] = 0.000325403; covariance[4, 4] = 0.001352532;

return covariance;

}

//

// hard-coded discount curve data

staticdouble[,] createDiscountCurve()

{

double[,] curve = newdouble[5, 2];

curve[0, 0] = 1.0; curve[0, 1] = 0.00285;

curve[1, 0] = 2.0; curve[1, 1] = 0.00425;

curve[2, 0] = 3.0; curve[2, 1] = 0.00761;

curve[3, 0] = 4.0; curve[3, 1] = 0.0119;

curve[4, 0] = 5.0; curve[4, 1] = 0.01614;

return curve;

}

//

// hard-coded cds curve data

staticdouble[,] createCDSCurve()

{

double[,] cds = newdouble[5, 5];

cds[0, 0] = 17.679; cds[0, 1] = 19.784;

cds[0, 2] = 11.242; cds[0, 3] = 23.5;

cds[0, 4] = 39.09; cds[1, 0] = 44.596;

cds[1, 1] = 44.921; cds[1, 2] = 27.737;

cds[1, 3] = 50.626; cds[1, 4] = 93.228;

cds[2, 0] = 54.804; cds[2, 1] = 64.873;

cds[2, 2] = 36.909; cds[2, 3] = 67.129;

cds[2, 4] = 107.847; cds[3, 0] = 83.526;

cds[3, 1] = 96.603; cds[3, 2] = 57.053;

cds[3, 3] = 104.853; cds[3, 4] = 164.815;

cds[4, 0] = 96.15; cds[4, 1] = 115.662;

cds[4, 2] = 67.82; cds[4, 3] = 118.643;

cds[4, 4] = 159.322;

return cds;

}

}

//

//

// *************************************************************

publicclassBasketCDS

{

public PremiumLegUpdate updatePremiumLeg; // delegate for sending value

public DefaultLegUpdate updateDefaultLeg; // delegate for sending value

private NAGCopula copula; // NAG copula model

private Func<double, double> df; // discounting method delegate

private CreditCurve cds; // credit curve

privateint k; // kth-to-default

privateint m; // number of reference assets

privateint n; // number of simulations

privateint maturity; // basket cds maturity in years (integer)

//

public BasketCDS(int kth, int simulations, int maturity, NAGCopula copula,

CreditCurve cds, Func<double, double> discountFactor)

{

this.k = kth;

this.n = simulations;

this.maturity = maturity;

this.copula = copula;

this.cds = cds;

this.df = discountFactor;

}

publicvoid Process()

{

// request correlated random numbers from copula model

int[] seed = newint[1] { Math.Abs(Guid.NewGuid().GetHashCode()) };

double[,] randomArray = copula.Create(n, seed);

m = randomArray.GetLength(1);

//

// process n sets of m correlated random numbers

for (int i = 0; i < n; i++)

{

// create a set of m random numbers needed for one simulation round

double[,] set = newdouble[1, m];

for (int j = 0; j < m; j++)

{

set[0, j] = randomArray[i, j];

}

//

// calculate default times for reference name set

calculateDefaultTimes(set);

}

}

privatevoid calculateDefaultTimes(double[,] arr)

{

// convert uniform random numbers into default times

int cols = arr.GetLength(1);

double[,] defaultTimes = newdouble[1, cols];

//

for (int j = 0; j < cols; j++)

{

// iteratively, find out the correct default tenor bucket

double u = arr[0, j];

double t = Math.Abs(Math.Log(1 - u));

//

for (int k = 0; k < cds.CumulativeHazardMatrix.GetLength(1); k++)

{

int tenor = 0;

double dt = 0.0; double defaultTenor = 0.0;

if (cds.CumulativeHazardMatrix[k, j] >= t)

{

tenor = k;

if (tenor >= 1)

{

// calculate the exact default time for a given reference name

dt = -(1 / cds.HazardMatrix[k, j]) * Math.Log((1 - u)

/ (Math.Exp(-cds.CumulativeHazardMatrix[k - 1, j])));

defaultTenor = tenor + dt;

//

// default time after basket maturity

if (defaultTenor >= maturity) defaultTenor = 0.0;

}

else

{

// hard-coded assumption

defaultTenor = 0.5;

}

defaultTimes[0, j] = defaultTenor;

break;

}

}

}

// proceed to calculate leg values

updateLegValues(defaultTimes);

}

privatevoid updateLegValues(double[,] defaultTimes)

{

// check for defaulted reference names, calculate leg values

// and send statistics updates for BasketCDSStatistics

int nDefaults = getNumberOfDefaults(defaultTimes);

if (nDefaults > 0)

{

// for calculation purposes, remove zeros and sort matrix

MatrixTools.RowMatrix_removeZeroValues(ref defaultTimes);

MatrixTools.RowMatrix_sort(ref defaultTimes);

}

// calculate and send values for statistics gatherer

double dl = calculateDefaultLeg(defaultTimes, nDefaults);

double pl = calculatePremiumLeg(defaultTimes, nDefaults);

updateDefaultLeg(dl);

updatePremiumLeg(pl);

}

privateint getNumberOfDefaults(double[,] arr)

{

int nDefaults = 0;

for (int i = 0; i < arr.GetLength(1); i++)

{

if (arr[0, i] > 0.0) nDefaults++;

}

return nDefaults;

}

privatedouble calculatePremiumLeg(double[,] defaultTimes, int nDefaults)

{

double dt = 0.0; double t; double p = 0.0; double v = 0.0;

if ((nDefaults > 0) && (nDefaults >= k))

{

for (int i = 0; i < k; i++)

{

if (i == 0)

{

// premium components from 0 to t1

dt = defaultTimes[0, i] - 0.0;

t = dt;

p = 1.0;

}

else

{

// premium components from t1 to t2, etc.

dt = defaultTimes[0, i] - defaultTimes[0, i - 1];

t = defaultTimes[0, i];

p = (m - i) / (double)m;

}

v += (df(t) * dt * p);

}

}

else

{

for (int i = 0; i < maturity; i++)

{

v += df(i + 1);

}

}

return v;

}

privatedouble calculateDefaultLeg(double[,] defaultTimes, int nDefaults)

{

double v = 0.0;

if ((nDefaults > 0) && (nDefaults >= k))

{

v = (1 - cds.Recovery) * df(defaultTimes[0, k - 1]) * (1 / (double)m);

}

return v;

}

}

//

//

// *************************************************************

publicclassCreditCurve

{

private Func<double, double> df;

privatedouble recovery;

privatedouble[,] CDSSpreads;

privatedouble[,] survivalMatrix;

privatedouble[,] hazardMatrix;

privatedouble[,] cumulativeHazardMatrix;

//

public CreditCurve(double[,] CDSSpreads,

Func<double, double> discountFactor, double recovery)

{

this.df = discountFactor;

this.CDSSpreads = CDSSpreads;

this.recovery = recovery;

createSurvivalMatrix();

createHazardMatrices();

}

// public read-only accessors to class data

publicdouble[,] HazardMatrix { get { returnthis.hazardMatrix; } }

publicdouble[,] CumulativeHazardMatrix { get { returnthis.cumulativeHazardMatrix; } }

publicdouble Recovery { get { returnthis.recovery; } }

//

privatevoid createSurvivalMatrix()

{

// bootstrap matrix of survival probabilities from given CDS data

int rows = CDSSpreads.GetUpperBound(0) + 2;

int cols = CDSSpreads.GetUpperBound(1) + 1;

survivalMatrix = newdouble[rows, cols];

//

double term = 0.0; double firstTerm = 0.0; double lastTerm = 0.0;

double terms = 0.0; double quotient = 0.0;

int i = 0; int j = 0; int k = 0;

//

for (i = 0; i < rows; i++)

{

for (j = 0; j < cols; j++)

{

if (i == 0) survivalMatrix[i, j] = 1.0;

if (i == 1) survivalMatrix[i, j] = (1 - recovery) / ((1 - recovery) + 1 * CDSSpreads[i - 1, j] / 10000);

if (i > 1)

{

terms = 0.0;

for (k = 0; k < (i - 1); k++)

{

term = df(k + 1) * ((1 - recovery) * survivalMatrix[k, j] -

(1 - recovery + 1 * CDSSpreads[i - 1, j] / 10000) * survivalMatrix[k + 1, j]);

terms += term;

}

quotient = (df(i) * ((1 - recovery) + 1 * CDSSpreads[i - 1, j] / 10000));

firstTerm = (terms / quotient);

lastTerm = survivalMatrix[i - 1, j] * (1 - recovery) / (1 - recovery + 1 * CDSSpreads[i - 1, j] / 10000);

survivalMatrix[i, j] = firstTerm + lastTerm;

}

}

}

}

privatevoid createHazardMatrices()

{

// convert matrix of survival probabilities into two hazard rate matrices

int rows = survivalMatrix.GetUpperBound(0);

int cols = survivalMatrix.GetUpperBound(1) + 1;

hazardMatrix = newdouble[rows, cols];

cumulativeHazardMatrix = newdouble[rows, cols];

int i = 0; int j = 0;

//

for (i = 0; i < rows; i++)

{

for (j = 0; j < cols; j++)

{

cumulativeHazardMatrix[i, j] = -Math.Log(survivalMatrix[i + 1, j]);

if (i == 0) hazardMatrix[i, j] = cumulativeHazardMatrix[i, j];

if (i > 0) hazardMatrix[i, j] = (cumulativeHazardMatrix[i, j] - cumulativeHazardMatrix[i - 1, j]);

}

}

}

}

//

//

// *************************************************************

publicclassDiscountCurve

{

// specific algorithms for interpolation and discounting

private InterpolationAlgorithm interpolationMethod;

private DiscountAlgorithm discountMethod;

privatedouble[,] curve;

//

public DiscountCurve(double[,] curve,

InterpolationAlgorithm interpolationMethod, DiscountAlgorithm discountMethod)

{

this.curve = curve;

this.interpolationMethod = interpolationMethod;

this.discountMethod = discountMethod;

}

publicdouble GetDF(double t)

{

// get discount factor from discount curve

return discountMethod(t, interpolation(t));

}

privatedouble interpolation(double t)

{

// get interpolation from discount curve

return interpolationMethod(t, refthis.curve);

}

}

//

//

// *************************************************************

// collection of methods for different types of mathematical operations

publicstaticclassMathTools

{

publicstaticdouble LinearInterpolation(double t, refdouble[,] curve)

{

int n = curve.GetUpperBound(0) + 1;

double v = 0.0;

//

// boundary checkings

if ((t < curve[0, 0]) || (t > curve[n - 1, 0]))

{

if (t < curve[0, 0]) v = curve[0, 1];

if (t > curve[n - 1, 0]) v = curve[n - 1, 1];

}

else

{

// iteration through all given curve points

for (int i = 0; i < n; i++)

{

if ((t >= curve[i, 0]) && (t <= curve[i + 1, 0]))

{

v = curve[i, 1] + (curve[i + 1, 1] - curve[i, 1]) * (t - (i + 1));

break;

}

}

}

return v;

}

publicstaticdouble ContinuousDiscountFactor(double t, double r)

{

return Math.Exp(-r * t);

}

}

//

//

// *************************************************************

// collection of methods for different types of matrix operations

publicstaticclassMatrixTools

{

publicstaticdouble[,] CorrelationToCovariance(double[,] corr, double[] stdev)

{

// transform correlation matrix to co-variance matrix

double[,] cov = newdouble[corr.GetLength(0), corr.GetLength(1)];

//

for (int i = 0; i < cov.GetLength(0); i++)

{

for (int j = 0; j < cov.GetLength(1); j++)

{

cov[i, j] = corr[i, j] * stdev[i] * stdev[j];

}

}

//

return cov;

}

publicstaticvoid RowMatrix_sort(refdouble[,] arr)

{

// sorting a given row matrix to ascending order

// input must be 1 x M matrix

// bubblesort algorithm implementation

int cols = arr.GetUpperBound(1) + 1;

double x = 0.0;

//

for (int i = 0; i < (cols - 1); i++)

{

for (int j = (i + 1); j < cols; j++)

{

if (arr[0, i] > arr[0, j])

{

x = arr[0, i];

arr[0, i] = arr[0, j];

arr[0, j] = x;

}

}

}

}

publicstaticvoid RowMatrix_removeZeroValues(refdouble[,] arr)

{

// removes zero values from a given row matrix

// input must be 1 x M matrix

List<double> temp = new List<double>();

int cols = arr.GetLength(1);

int counter = 0;

for (int i = 0; i < cols; i++)

{

if (arr[0, i] > 0)

{

counter++;

temp.Add(arr[0, i]);

}

}

if (counter > 0)

{

arr = newdouble[1, temp.Count];

for (int i = 0; i < temp.Count; i++)

{

arr[0, i] = temp[i];

}

}

else

{

arr = null;

}

}

}

//

//

// *************************************************************

// NAG G05 COPULAS WRAPPER

publicclassNAGCopula

{

privatedouble[,] covariance;

privateint genID;

privateint subGenID;

privateint mode;

privateint df;

privateint m;

privateint errorNumber;

privatedouble[] r;

privatedouble[,] result;

//

public NAGCopula(double[,] covariance, int genID,

int subGenID, int mode, int df = 0)

{

// ctor : create correlated uniform random numbers

// degrees-of-freedom parameter (df), being greater than zero,

// will automatically trigger the use of student copula

this.covariance = covariance;

this.genID = genID;

this.subGenID = subGenID;

this.mode = mode;

this.df = df;

this.m = covariance.GetLength(1);

r = newdouble[m * (m + 1) + (df > 0 ? 2 : 1)];

}

publicdouble[,] Create(int n, int[] seed)

{

result = newdouble[n, m];

//

G05.G05State g05State = new G05.G05State(genID, subGenID, seed, out errorNumber);

if (errorNumber != 0) thrownew Exception("G05 state failure");

//

if (this.df != 0)

{

// student copula

G05.g05rc(mode, n, df, m, covariance, r, g05State, result, out errorNumber);

}

else

{

// gaussian copula

G05.g05rd(mode, n, m, covariance, r, g05State, result, out errorNumber);

}

//

if (errorNumber != 0) thrownew Exception("G05 method failure");

return result;

}

}

//

//

// *************************************************************

publicclassStatistics

{

// data structures for storing leg values

private List<double> premiumLeg;

private List<double> defaultLeg;

privatestring ID;

//

public Statistics(string ID)

{

this.ID = ID;

premiumLeg = new List<double>();

defaultLeg = new List<double>();

}

publicvoid UpdatePremiumLeg(double v)

{

premiumLeg.Add(v);

}

publicvoid UpdateDefaultLeg(double v)

{

defaultLeg.Add(v);

}

publicvoid PrettyPrint()

{

// hard-coded 'report' output

Console.WriteLine("{0} : {1} bps", ID, Math.Round(Spread() * 10000, 2));

}

publicdouble Spread()

{

return defaultLeg.Average() / premiumLeg.Average();

}

}

}

/pic9729642.png)