Third-party analytics softwares will usually require a full set of market data to be feeded into system, before performing any of those precious high intensity calculations. Market data (curves, surfaces, fixing time-series, etc.) has to be feeded into system following some specific file configurations. Moreover, source data might have to be collected from several different vendor sources. Needless to say, the process can easily turn into a semi-manageable mess involving Excel workbooks and a lot of manual processing, which is always a bad omen.

For this reason, I finally ended up creating one possible design solution for flexible processing of market data files. I have been going through some iterations starting with Abstract Factory, before landing with the current one using Delegates to pair data and algorithms. With the current solution, I start to feel quite comfortable already.

![]()

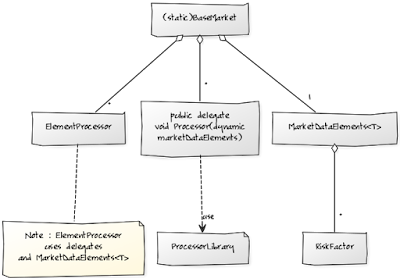

Each market data point (such as mid USD swap rate for 2 years) is presented as a RiskFactor object. All individual RiskFactor objects are hosted in a list inside generic MarketDataElements<T> object, which enables hosting any type of data. MarketDataElements<T> object itself is hosted by static BaseMarket class.

The actual algorithms needed for creating any type of vendor data are captured in static ProcessorLibrary class. During the processing task, MarketDataElements<T> object will be handled for a specific library method implementation, which will then request values from vendor source for all involved RiskFactor objects. In the example program, ProcessorLibrary has a method for processing RiskFactor objects using Bloomberg market data API. This specific method is then using DummyBBCOMMWrapper class for requesting values for a RiskFactor object.

For the purpose of pairing specific data (MarketDataElements<T>) and specific algorithm (ProcessorLibrary), BaseMarket class is hosting a list of ElementProcessor objects as well as a list of Delegates bound with specific methods found in ProcessorLibrary. For the processing task, each ElementProcessor object is feeded with delegate method for specific ProcessorLibrary implementation method and information on MarketDataElements<T> object.

Finally, (not shown in UML) program is also using static TextFileHandler class for handling text files and static Configurations class for hosting hardcoded configurations, initially read from App.config file.

![]()

CSV for all RiskFactor object configurations

Fields (matching with RiskFactor object properties) :

![]()

Result CSV

![]()

Create a new console project and CopyPaste the following program into corresponding CS files. When testing the program in a real production environment, just add reference to Bloomberg API DLL file and replace DummyBBCOMMWrapper class with this.

Adding a new data vendor processor XYZ involves the following four easy steps :

-Mike

For this reason, I finally ended up creating one possible design solution for flexible processing of market data files. I have been going through some iterations starting with Abstract Factory, before landing with the current one using Delegates to pair data and algorithms. With the current solution, I start to feel quite comfortable already.

UML

Each market data point (such as mid USD swap rate for 2 years) is presented as a RiskFactor object. All individual RiskFactor objects are hosted in a list inside generic MarketDataElements<T> object, which enables hosting any type of data. MarketDataElements<T> object itself is hosted by static BaseMarket class.

The actual algorithms needed for creating any type of vendor data are captured in static ProcessorLibrary class. During the processing task, MarketDataElements<T> object will be handled for a specific library method implementation, which will then request values from vendor source for all involved RiskFactor objects. In the example program, ProcessorLibrary has a method for processing RiskFactor objects using Bloomberg market data API. This specific method is then using DummyBBCOMMWrapper class for requesting values for a RiskFactor object.

For the purpose of pairing specific data (MarketDataElements<T>) and specific algorithm (ProcessorLibrary), BaseMarket class is hosting a list of ElementProcessor objects as well as a list of Delegates bound with specific methods found in ProcessorLibrary. For the processing task, each ElementProcessor object is feeded with delegate method for specific ProcessorLibrary implementation method and information on MarketDataElements<T> object.

Finally, (not shown in UML) program is also using static TextFileHandler class for handling text files and static Configurations class for hosting hardcoded configurations, initially read from App.config file.

Files

App.config

CSV for all RiskFactor object configurations

Fields (matching with RiskFactor object properties) :

- Data vendor identification string, matching with the one given in configuration file

- Identification code (ticker) for a market data element, found in the system for which the data will be created

- Vendor ticker for a market data element (Bloomberg ISIN code)

- Field name for a market data element (Bloomberg field PX_MID)

- Divider (Bloomberg is presenting a rate as percentage 1.234, but target system may need to have an input as absolute value 0.01234)

- Empty field for a value to be processed by specific processor implementation for specific data vendor.

Result CSV

The program

Create a new console project and CopyPaste the following program into corresponding CS files. When testing the program in a real production environment, just add reference to Bloomberg API DLL file and replace DummyBBCOMMWrapper class with this.

Adding a new data vendor processor XYZ involves the following four easy steps :

- Update providers in App.config file : <add key="RiskFactorDataProviders" value="BLOOMBERG,XYZ" />

- Create a new method implementation into ProcessorLibrary : public static void ProcessXYZRiskFactors(dynamic marketDataElements) { // implement algorithm}

- Add selection for a new processor into BaseMarket class method createElementProcessors: if(dataProviderString.ToUpper() == "XYZ") elementProcessors.Add(new ElementProcessor(ProcessorLibrary.ProcessXYZRiskFactors, elements));

- Create new RiskFactor object configurations into source file for a new vendor XYZ

-Mike

// MainProgram.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.Linq;

usingSystem.Text;

namespaceMarketDataProcess

{

classMainProgram

{

staticvoidMain(string[] args)

{

try

{

// process base market risk factors to file

BaseMarket.Process();

BaseMarket.PrintToFile();

}

catch (Exception e)

{

Console.WriteLine(e.Message);

}

}

}

}

//

//

//

//

// BaseMarket.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.Linq;

usingSystem.Text;

namespaceMarketDataProcess

{

// class for administrating risk factors and processors for base market

publicstaticclassBaseMarket

{

privatestatic List<string> inputFileStreams = new List<string>();

privatestatic MarketDataElements<RiskFactor> riskFactors = new MarketDataElements<RiskFactor>();

privatestatic List<ElementProcessor> elementProcessors = new List<ElementProcessor>();

privatestaticint nRiskFactors = 0;

//

publicstaticvoidProcess()

{

// read all source data string streams from file into list

TextFileHandler.Read(Configurations.BaseMarketSourceDataFilePathName, inputFileStreams);

//

// extract string streams and create risk factor objects

foreach (string inputFileStream in inputFileStreams)

{

RiskFactor element = new RiskFactor();

element.Create(inputFileStream);

riskFactors.AddElement(element);

}

nRiskFactors = riskFactors.elements.Count;

//

// create and execute market data element processors

// finally run technical check on created risk factors

BaseMarket.createElementProcessors();

elementProcessors.ForEach(processor => processor.Process());

BaseMarket.Check();

}

publicstaticvoidPrintToFile()

{

// write created base market risk factors into file

StringBuilder stream = new StringBuilder();

for (int i = 0; i < riskFactors.elements.Count; i++)

{

stream.AppendLine(String.Format("{0},{1}", riskFactors.elements[i].systemTicker, riskFactors.elements[i].value));

}

TextFileHandler.Write(Configurations.BaseMarketResultDataFilePathName, stream.ToString(), false);

}

privatestaticvoidcreateElementProcessors()

{

// market data element processor types are defined in configuration file

List<string> dataProviderStrings = Configurations.RiskFactorDataProviders.Split(',').ToList<string>();

//

foreach (string dataProviderString in dataProviderStrings)

{

if (dataProviderString == String.Empty) thrownew Exception("No element processor defined");

List<RiskFactor> elements = riskFactors.elements.Where(factor => factor.provider == dataProviderString).ToList<RiskFactor>();

if(dataProviderString.ToUpper() == "BLOOMBERG") elementProcessors.Add(new ElementProcessor(ProcessorLibrary.ProcessBloombergRiskFactors, elements));

}

}

publicstatic MarketDataElements<RiskFactor> GetRiskFactors()

{

// create and return deep copy of all base market risk factors

return riskFactors.Clone();

}

privatestaticvoidCheck()

{

int nValidRiskFactors = 0;

//

// loop through all created risk factors for base market

for (int i = 0; i < riskFactors.elements.Count; i++)

{

// extract risk factor to be investigated for valid value

RiskFactor factor = riskFactors.elements[i];

//

// valid value inside risk factor should be double-typed converted to string, ex. "0.05328"

// check validity of this value with Double

// TryParse-method returning TRUE if string value can be converted to double

doublevalue = 0;

bool isValid = Double.TryParse(factor.value, outvalue);

if (isValid) nValidRiskFactors++;

//

// if value is not convertable to double, get user input for this value

if (!isValid)

{

while (true)

{

Console.Write(String.Format("Provide input for {0} >", factor.systemTicker));

bool validUserInput = Double.TryParse(Console.ReadLine(), outvalue);

if (validUserInput)

{

factor.value = value.ToString();

nValidRiskFactors++;

break;

}

else

{

// client is forced to set (at least technically) valid value

Console.WriteLine("Invalid value, try again");

}

}

}

}

}

}

}

//

//

//

//

// Configurations.cs

usingSystem;

usingSystem.Configuration;

namespaceMarketDataProcess

{

// static class for hosting configurations

publicstaticclassConfigurations

{

// readonly data for public sharing

publicstaticreadonlystring RiskFactorDataProviders;

publicstaticreadonlystring BaseMarketSourceDataFilePathName;

publicstaticreadonlystring BaseMarketResultDataFilePathName;

//

// private constructor will be called just before any configuration is requested

staticConfigurations()

{

// configuration strings are assigned to static class data members for easy access

RiskFactorDataProviders = ConfigurationManager.AppSettings["RiskFactorDataProviders"].ToString();

BaseMarketSourceDataFilePathName = ConfigurationManager.AppSettings["BaseMarketSourceDataFilePathName"].ToString();

BaseMarketResultDataFilePathName = ConfigurationManager.AppSettings["BaseMarketResultDataFilePathName"].ToString();

}

}

}

//

//

//

//

// MarketDataElement.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.Linq;

namespaceMarketDataProcess

{

// generic template for all types of market data elements (risk factors, fixings)

publicclassMarketDataElements<T> where T : ICloneable, new()

{

public List<T> elements = new List<T>();

publicvoidAddElement(T element)

{

elements.Add(element);

}

public MarketDataElements<T> Clone()

{

// create a deep copy of market data elements object

MarketDataElements<T> clone = new MarketDataElements<T>();

//

// copy content for all elements into a list

List<T> elementList = new List<T>();

foreach (T element in elements)

{

elementList.Add((T)element.Clone());

}

clone.elements.AddRange(elementList);

return clone;

}

}

// risk factor as market data element

publicclassRiskFactor : ICloneable

{

publicstring provider;

publicstring systemTicker;

publicstring vendorTicker;

publicstring vendorField;

publicstring divider;

publicstringvalue;

//

publicRiskFactor() { }

publicvoidCreate(string stream)

{

List<string> fields = stream.Split(',').ToList<string>();

this.provider = fields[0];

this.systemTicker = fields[1];

this.vendorTicker = fields[2];

this.vendorField = fields[3];

this.divider = fields[4];

this.value = fields[5];

}

publicobjectClone()

{

RiskFactor clone = new RiskFactor();

clone.provider = this.provider;

clone.systemTicker = this.systemTicker;

clone.vendorTicker = this.vendorTicker;

clone.vendorField = this.vendorField;

clone.divider = this.divider;

clone.value = this.value;

return clone;

}

}

// fixing as market data element

publicclassFixing : ICloneable

{

publicstring provider;

publicstring systemTicker;

publicstring vendorTicker;

publicstring vendorField;

publicstring frequency;

publicstring nYearsBack;

publicstring divider;

publicstringvalue;

public Dictionary<string, string> timeSeries = new Dictionary<string, string>();

//

publicFixing() { }

publicvoidCreate(string stream)

{

List<string> fields = stream.Split(',').ToList<string>();

this.provider = fields[0];

this.systemTicker = fields[1];

this.vendorTicker = fields[2];

this.vendorField = fields[3];

this.frequency = fields[4];

this.nYearsBack = fields[5];

this.divider = fields[6];

this.value = fields[7];

}

publicobjectClone()

{

Fixing clone = new Fixing();

clone.provider = this.provider;

clone.systemTicker = this.systemTicker;

clone.vendorTicker = this.vendorTicker;

clone.vendorField = this.vendorField;

clone.divider = this.divider;

clone.value = this.value;

//

// create deep copy of timeseries dictionary

Dictionary<string, string> timeSeriesClone = new Dictionary<string, string>();

foreach (KeyValuePair<string, string> kvp inthis.timeSeries)

{

timeSeriesClone.Add(kvp.Key, kvp.Value);

}

clone.timeSeries = timeSeriesClone;

return clone;

}

}

}

//

//

//

//

// ElementProcessor.cs

usingSystem;

usingSystem.Collections.Generic;

namespaceMarketDataProcess

{

// algorithm for creating market data element objects

publicdelegatevoidProcessor(dynamic marketDataElements);

//

// class for hosting data and algorithm

publicclassElementProcessor

{

private Processor taskProcessor;

dynamic marketDataElements;

publicElementProcessor(Processor taskProcessor, dynamic marketDataElements)

{

this.taskProcessor = taskProcessor;

this.marketDataElements = marketDataElements;

}

publicvoidProcess()

{

taskProcessor.Invoke(marketDataElements);

}

}

}

//

//

//

//

// ProcessorLibrary.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.Linq;

namespaceMarketDataProcess

{

publicstaticclassProcessorLibrary

{

publicstaticvoidProcessBloombergRiskFactors(dynamic marketDataElements)

{

List<RiskFactor> riskFactors = (List<RiskFactor>)marketDataElements;

BBCOMMWrapper.BBCOMMDataRequest request;

dynamic[, ,] result = null;

string SYSTEM_DOUBLE = "System.Double";

int counter = 0;

//

// group data list into N lists grouped by distinct bloomberg field names

var dataGroups = riskFactors.GroupBy(factor => factor.vendorField);

//

// process each group of distinct bloomberg field names

for (int i = 0; i < dataGroups.Count(); i++)

{

// extract group, create data structures for securities and fields

List<RiskFactor> dataGroup = dataGroups.ElementAt(i).ToList<RiskFactor>();

List<string> securities = new List<string>();

List<string> fields = new List<string>() { dataGroup[0].vendorField };

//

// import securities into data structure feeded to bloomberg api

for (int j = 0; j < dataGroup.Count; j++)

{

securities.Add(dataGroup[j].vendorTicker);

}

//

// create and use request object to retrieve bloomberg data

request = new BBCOMMWrapper.ReferenceDataRequest(securities, fields);

result = request.ProcessData();

//

// write retrieved bloomberg data into risk factor group data

for (int k = 0; k < result.GetLength(0); k++)

{

string stringValue;

dynamicvalue = result[k, 0, 0];

//

if (value.GetType().ToString() == SYSTEM_DOUBLE)

{

// handle output value with divider only if retrieved value is double

// this means that data retrieval has been succesfull

double divider = Convert.ToDouble(dataGroup[k].divider);

stringValue = (value / divider).ToString();

dataGroup[k].value = stringValue;

counter++;

}

else

{

// write non-double value (bloomberg will retrieve #N/A) if retrieved value is not double

stringValue = value.ToString();

dataGroup[k].value = stringValue;

}

}

}

}

}

}

//

//

//

//

// DummyBBCOMMWrapper.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.Linq;

usingSystem.Text;

usingSystem.Threading.Tasks;

namespaceBBCOMMWrapper

{

// abstract base class for data request

publicabstractclassBBCOMMDataRequest

{

// input data structures

protected List<string> securityNames = new List<string>();

protected List<string> fieldNames = new List<string>();

//

// output result data structure

protecteddynamic[, ,] result;

//

publicdynamic[, ,] ProcessData()

{

// instead of the actual Bloomberg market data, random numbers are going to be generated

Random randomGenerator = new Random(Math.Abs(Guid.NewGuid().GetHashCode()));

//

for (int i = 0; i < securityNames.Count; i++)

{

for (int j = 0; j < fieldNames.Count; j++)

{

result[i, 0, j] = randomGenerator.NextDouble();

}

}

return result;

}

}

//

// concrete class implementation for processing reference data request

publicclassReferenceDataRequest : BBCOMMDataRequest

{

publicReferenceDataRequest(List<string> bloombergSecurityNames,

List<string> bloombergFieldNames)

{

securityNames = bloombergSecurityNames;

fieldNames = bloombergFieldNames;

result = newdynamic[securityNames.Count, 1, fieldNames.Count];

}

}

}

//

//

//

//

// TextFileHandler.cs

usingSystem;

usingSystem.Collections.Generic;

usingSystem.IO;

namespaceMarketDataProcess

{

publicstaticclassTextFileHandler

{

publicstaticvoidRead(string filePathName, List<string> output)

{

// read file content into list

StreamReader reader = new StreamReader(filePathName);

while (!reader.EndOfStream)

{

output.Add(reader.ReadLine());

}

reader.Close();

}

publicstaticvoidWrite(string filePathName, List<string> input, bool append)

{

// write text stream list to file

StreamWriter writer = new StreamWriter(filePathName, append);

input.ForEach(it => writer.WriteLine(it));

writer.Close();

}

publicstaticvoidWrite(string filePathName, string input, bool append)

{

// write bulk text stream to file

StreamWriter writer = new StreamWriter(filePathName, append);

writer.Write(input);

writer.Close();

}

}

}